Still Renting Because You Believe the Wrong Rule?

Still Renting Because You Believe the Wrong Rule?

Click Here for a complete Guide to USDA Loans (PDF) -

Most people think buying a house starts with one thing: a big down payment. That belief alone is keeping people stuck renting for years longer than they should be, because it’s not true.

There is a loan that allows you to buy a home with 0% down. It means no massive savings account, no waiting five more years, and no putting your life on hold. It’s called a USDA loan, and understanding how to structure it can change everything.

The Part No One Explains

The Part No One Explains

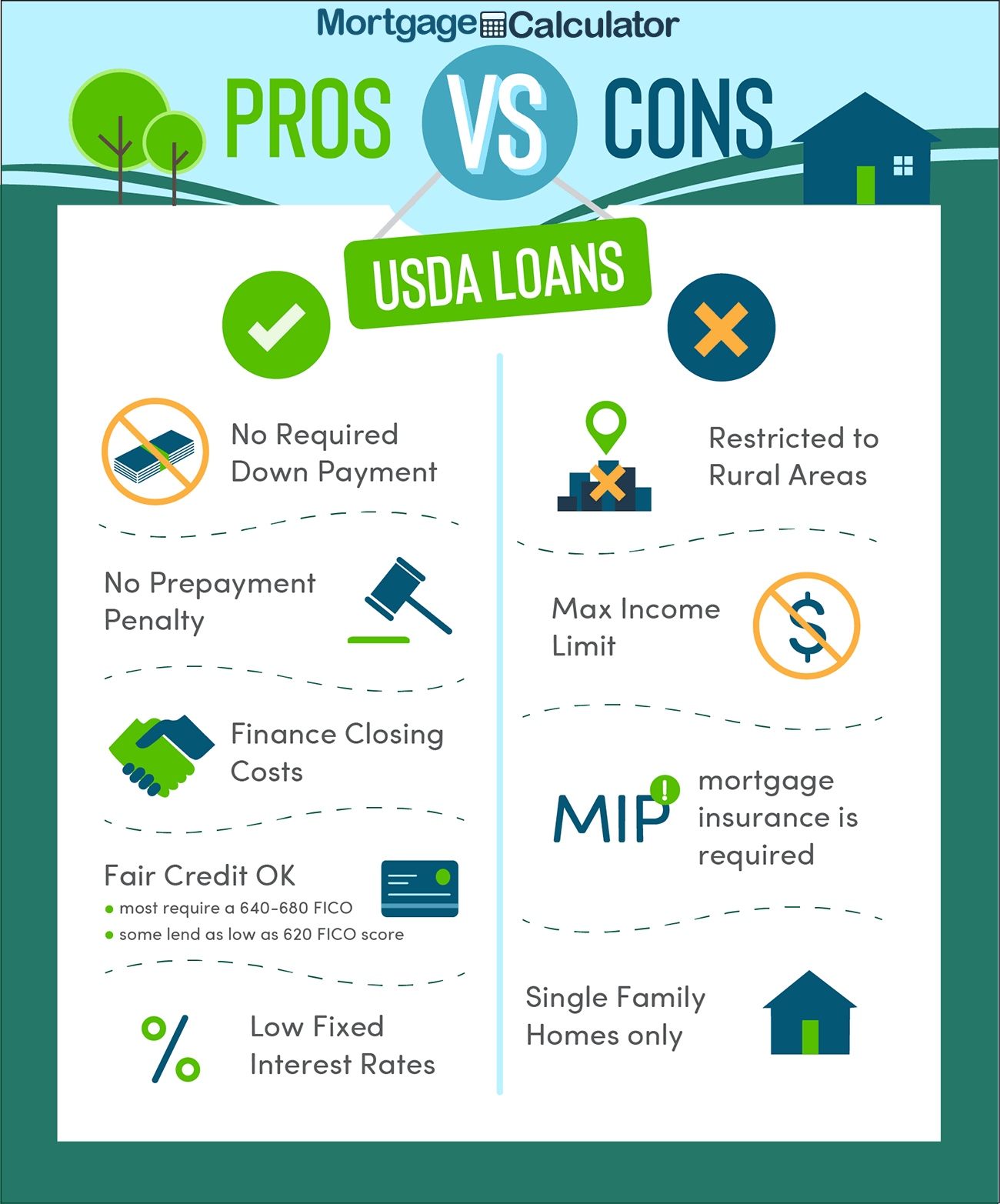

Yes, USDA allows you to buy with zero down….that’s real. However, most people assume “no down payment” means “no money needed at all,” which is not quite right.

You still have closing costs, usually somewhere between 2% and 5% of the purchase price. These costs include things like lender fees, title work, and prepaid items.

Here is the part most people don’t know: you can often get the seller to pay those costs for you. USDA actually allows up to a 6% seller contribution. Since closing costs are typically 2% to 5% and the seller can pay up to 6%, it is absolutely possible to walk into a house with little to nothing out of pocket.

Where Deals Are Won or Lost

The real game is knowing how to structure the deal so you don’t have to bring cash to the table. For this to work, several conditions must be met:

- The home has to appraise

- The numbers have to be clean

- The offer has to be written the right way

- The seller has to agree

The truth is, most people don’t know how to put that together, so buyers assume they need $10K, $15K, or $20K saved, and they keep renting. We need to get the sellers to cover your closing cost!

What a USDA Loan Actually Is

At its core, a USDA loan is a government-backed loan designed to help people buy homes in eligible areas. It’s a misconception that it's just for farmland; a lot of areas around Savannah (West of I-95) and surrounding communities, for example, qualify.

Basic requirements for the loan include:

- You must live in the home (primary residence only)

- Your income must fall within limits (generally under about 115% of the area median)

- The home must be in an eligible location (WEST OF I-95)

- The property must be move-in ready

Credit, Income, and What They’re Looking For

While it’s not a “free pass” loan and you still need to qualify, it is more flexible than most people think.

A 640+ credit score is ideal

- Lower scores can work, but the process gets tougher

- Debt-to-income is usually around 41%

- Lenders are not looking for perfection; they are looking for consistency, paying your bills, managing your debt, and showing you can handle a mortgage.

Costs (And Why This Loan Still Wins)

USDA loans do not have the traditional PMI required by FHA loans. Instead, they have two fees:

An upfront fee (about 1%) is usually rolled into the loan

A small annual fee (about 0.35%) is built into your monthly payment

In most cases, your monthly cost with a USDA loan is lower than with an FHA loan. Rates are also typically competitive, and sometimes even better depending on the situation.

Biggest Mistake

The biggest mistake people make is waiting. They wait to save more, they wait for rates to drop, or they wait until they feel “ready”. Meanwhile, they are paying rent every month, building zero equity, and missing opportunities sitting right in front of them.

Right now, in this market, buyers have leverage, which means:

- Sellers are more open to concessions (paying all your closing costs)

- Deals can be negotiated (paying all your closing costs)

- Closing costs can be covered (paying all your closing costs)

- Get it, the time is perfect for… negotiating for a lower purchase price and the seller to pay all your closing costs!

But that window doesn’t stay open forever.

Who This Works Best For

This loan is perfect if:

- You have a steady income

- You don’t have a large down payment saved

- You’re open to eligible areas

- You want to get in now instead of waiting years

It is not for fixer-uppers or for investors. But for the right buyer, it’s one of the strongest plays out there.

Bottom Line

You don’t need a massive down payment to buy a house. You need the right strategy. USDA is one of the few paths where you can realistically get in with little to nothing out of pocket—if it’s structured correctly. Most people never even realize it’s an option.

Categories

Recent Posts

GET MORE INFORMATION