Are Middle-Class And First-Time Homeowners Being Priced Out Of Home Ownership?

Here's some straight talk about the housing market! It's getting harder and harder for the middle class to live the American Dream of owning a home. With mortgage interest rates at their highest in decades, high inflation, and skyrocketing home prices, you need a solid plan when buying a house! The days of 3.0% interest rates are gone, if not forever, for a long time. But home ownership is still possible if you know how to get there.

Typically, homeowners have 40x the net worth of their friends who rent! Some renters assume they don't pay for the maintenance of their rental…but they do! It’s just built into the rent! If nothing needs fixing during the lease term, the landlord keeps that money as a bonus!

So, how can you get to home ownership in this market?

Government Incentives

Government incentives, such as down payment assistance and $10,000 towards closing costs, aim to support first-time homebuyers. These programs increase the number of people who can afford to buy a home. In a sense, it's free money for the home purchase. Buyers who use these programs can significantly reduce the cost of a home.

First-Time Homebuyer Down Payment and ZERO DOWN Mortgage Programs

First-time homebuyer down payment and zero down mortgage programs are designed to eliminate the burden of the down payment. These programs often provide grants, low-interest loans, or deferred payment loans to help cover the down payment and, in some cases, closing costs. Eligibility requirements typically include being a first-time homebuyer, meeting income and home price limits, and completing a homebuyer education course. These programs make homeownership more accessible, providing an excellent resource for those buying their first home.

Loan Types and Seller Contributions

Homebuyers can also take advantage of seller contributions, which cover closing costs, prepaid items, and discount points. This reduces the amount of cash buyers need to bring to the table. These contributions make purchasing a home more affordable for first-time and other home buyers by lowering the initial out-of-pocket cash. Considering different loan types and understanding the various down-payment and allowable seller contributions will keep thousands of dollars in your pocket. Depending on your chosen loan, you can get between 1% to 9% of the sale price as a seller contribution.

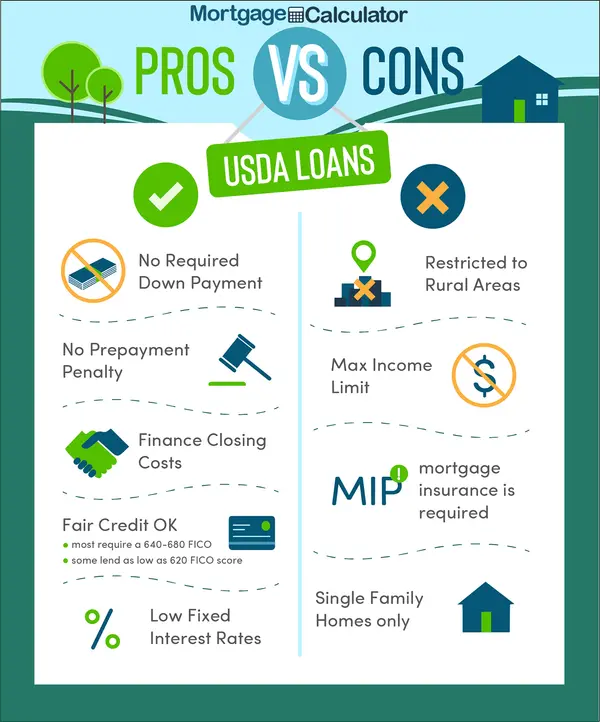

USDA Loans

USDA loans are another valuable option for first-time homebuyers, particularly those looking to buy in rural and suburban areas. These loans, backed by the U.S. Department of Agriculture, offer benefits such as no down payment, low interest rates, and flexible credit requirements. They provide an opportunity for eligible buyers to own a home with favorable financing terms.

Mortgage Buydowns

How would you like a 4% mortgage today? If so, consider mortgage buydowns. This strategy allows buyers or third parties (like sellers or builders) to pay an upfront fee to the lender to reduce the interest rate on a mortgage. The discount can be temporary or permanent. Buydowns make monthly payments more affordable, especially during the beginning years of the loan. By providing lower initial payments, buydowns are particularly useful for first-time buyers who expect their income to increase

DSCR Loans for Investment Properties

House HACK!? You can buy a multi-unit building like a duplex or larger, live in one unit, and let your tenants pay your mortgage. This puts money in your pocket! DSCR (Debt Service Coverage Ratio) loans are an excellent option for those considering investment properties. These loans focus on the property's income-generating potential rather than the borrower's personal income. DSCR loans are particularly attractive for real estate investors who might not qualify for traditional financing. The primary qualification is the income generated by the property, making it easier for investors with unverifiable income or complicated financial situations to secure financing.

Hedge Funds and Single-Family Homes

Hedge funds and institutional investors have been increasingly active in the single-family home market. By June 2022, large hedge funds and institutional investors held approximately 574,000 single-family homes in the U.S., accounting for a significant portion of the market. In some markets, these investors purchase up to 30% of available homes, often outbidding traditional buyers and driving up prices. This trend highlights the importance of government programs and strategies like mortgage buydowns to help individual buyers compete. If these institutions are buying up single-family homes, you should too.

The Importance of Professional Guidance When Buying Your First Home

In the current market, first-time homebuyers should consider a few compromises, like a smaller home that may not be in an ideal location or meet all their criteria. Even if a home isn't perfect, owning it is more beneficial in the long run than renting. Remember, homeowners have a net worth 40 times greater than renters.

Navigating today's complex real estate market requires expertise and help to develop a long-term plan. Gone are the days of easily securing a 3% mortgage and affording a $600,000 home. Strategic planning and professional guidance are now essential for making informed decisions. You need an expert to help you find and take advantage of government incentives and programs for first-time homebuyers. First-time buyers need a seasoned veteran to advise them about all the options like USDA loans, mortgage buydowns, and DSCR loans for investment properties. Remember, owning a home boosts your net worth significantly, making it a wiser financial decision than renting over the long run.

Categories

Recent Posts

GET MORE INFORMATION